Since May 2022, the Reserve Bank of Australia has lifted the cash rate from a historic low of 0.10% to 4.35% through one of the sharpest tightening cycles in its modern history. A brief easing phase through 2025 offered some relief, but three further increases in early 2026 have fully unwound those cuts. With headline inflation continuing to accelerate and underlying inflation remaining above the RBA’s 2–3% target band, further respite is not assured. Business owners would be wise to plan around a sustained period of elevated rates.

For most business owners, the impact has been felt directly through rising loan repayments and tighter cash flow. What is less understood is the parallel effect on business valuations. Even well-performing businesses might see their estimated value decline and understanding why requires a look at a fundamental valuation principle.

Why interest rates affect what your business is worth

A business is broadly worth the cash flows it is expected to generate in the future, expressed in today’s dollars. To bring future earnings into a present-day figure, valuers apply a discount rate. Think of it as the rate of return an investor would require to choose your business over other available investments. The higher that required return, the less they are willing to pay upfront for the same future earnings.

This plays out in a few ways:

- Inflated borrowing costs for businesses increase the cost of funding (debt repayments) and reduce profit margins. Since 2022, borrowing costs have risen sharply.

- Funders, utilising both equity and debt, should now be demanding higher investment returns, as they can now generate a higher risk-free return from lower risk options like government bonds or diversified portfolios.

- Higher rates also reduce household disposable income, which weighs most heavily on businesses reliant on discretionary consumer spending.

The first two direct effects push the discount (cost of capital) rate up. A higher discount rate in isolation implies a relatively lower valuation for any business or asset.

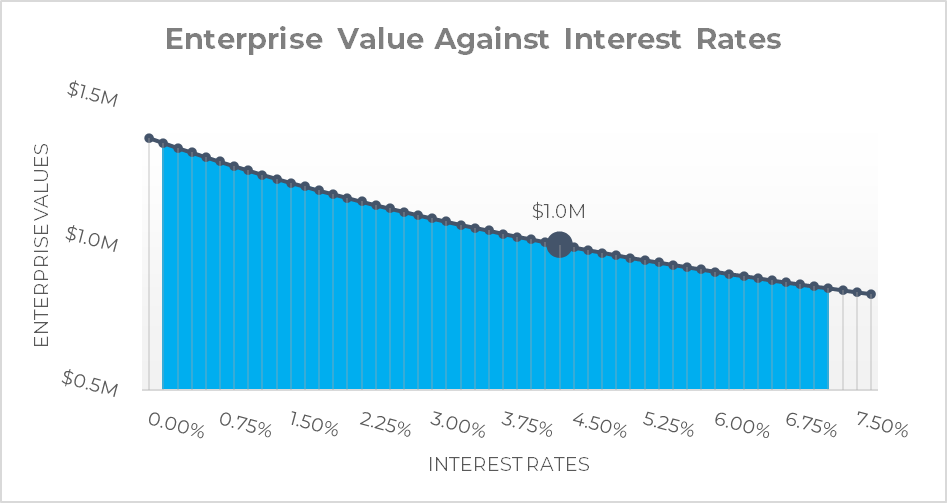

The same business, a lower number

Note: The marker identifies the enterprise value of the sample business as of May 2026, and the shaded blue region identifies the potential valuation range given Australian interest rates over the last 20 years.

Consider the graph. The total enterprise value is the present value of the cash flows that a business’s operating assets are expected to generate for both debt and equity holders. As the cost of capital rises, that present value falls, even when the underlying earnings of the business have not changed 1. In other words, the economic climate at the time of valuation is as significant a factor as the operating performance of the business itself.

Not all businesses are equally exposed

The impact of rising rates on business valuations varies across different industries and business types.

- Growth-oriented businesses, where lots of value sits in earnings several years into the future, are more sensitive to rate movements than stable, short-term cash-generative businesses. The compounding effect of a higher discount rate is further amplified the farther out those future cash flows sit. Here in Australia, this is particularly relevant for start-ups and other long-term growth-based businesses.

- Businesses servicing variable rate loans face a compounding problem. Higher rates compress valuation while also lifting actual debt servicing costs, which reduces the earnings base on which the equity valuation is calculated.

- By contrast, asset-backed businesses, that is those with material plant and equipment, especially property, or land, tend to be better insulated. Tangible asset values tend to provide a floor valuation price and often face less volatility than pure earnings-based businesses.

What this means for business owners right now

- If you are looking to sell, understand that SME valuations operate on different mechanics to the listed market. Public equities are easily traded, but private business sales typically rely on a single buyer often funding the purchase with debt. As rates rise, that buyer’s serviceability falls. Both the pool of viable buyers shrinks, and the price they can feasibly offer comes down.

- If you are looking to acquire, entry valuations have improved, but acquisition financing is more expensive. With markets pricing in the possibility of further increases through 2026, modelling acquisitions requires refreshed expectations.

Interest rates are one of the most significant external factors affecting what your business is worth today. Whether you are considering a sale, exploring an acquisition or simply want a clear picture of your current valuation, our Corporate Finance team can help you navigate the numbers.

1Calculated using the WACC formula, with assumed equity value of $250k, beta of 1, alpha of ~15.75%, D/V mix of 20%, market risk premium of 4.5%, corporate tax rate of 25% and a credit spread of 2.75%.

About the Author

Thomas Minns

Analyst, Corporate Finance, South Australia

Thomas is an analyst in the corporate finance team based in Adelaide, South Australia, led by Grant Miles. He has several years of corporate finance and consulting experience, holding a Bachelor of Economics (B. Econ) and Finance (B. Fin) from the University of Adelaide.

Contact Us

Contact our Corporate Finance team to discuss your situation.